Table of Content

This compensation may impact how and where products appear on this site . PrimeRates strives to provide a wide array of offers, but our offers do not represent all financial services companies or products. Lenders can allow co-signers on a home equity loan, and in some instances, it may be to your advantage to have someone co-sign. If that person has a strong credit score, low debt, and steady income, it could help to offset any shortcomings in your own credit history. Keep in mind, however, that the co-signer becomes equally responsible for the debt, and it will show up on their credit history.

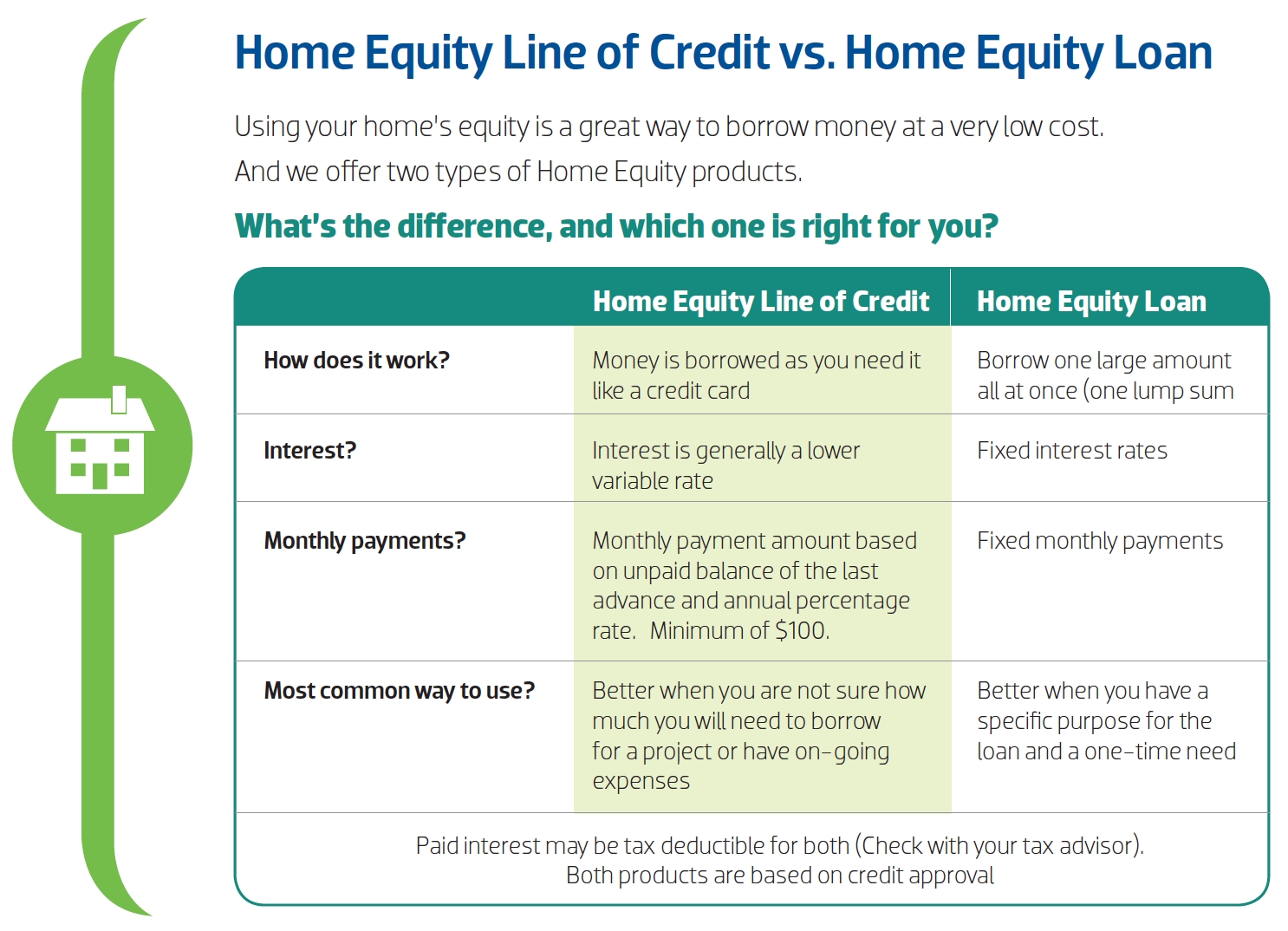

A home equity loan pays one lump sum, while a HELOC remains as an open line of credit for a set period of time. Home equity loan payments work in a similar fashion to mortgage loan payments. Co-signers often make the same mistake as borrowers, assuming that the lender will simply take the house if the loan isn't paid. Some view co-signing on a mortgage or home equity loan as much less dangerous than doing so on a car loan or personal loan. As is true of all co-signing situations, the lender will attempt to collect the debt from both the borrower and co-signer. If the borrower defaults, the bank will pursue the co-signer for the money.

Business Loans for Black Women Entrepreneurs

Make sure you and your co-signer are comfortable with agreeing to such a serious, long-term financial arrangement. Also, be certain your co-signer understands that their credit score is on the line, as it will drop if you miss payments. When you fill out the application, include the co-signer's information. Indicate that the property is in your name, but the loan will be to both of you. Submit your application along with financial information for both yourself and the co-signer. The co-signer will sign all applicable disclosures and authorize the lender to run his credit report.

Although lenders want your DTI ratio to stay below 43 percent, if you have bad credit, the lower the ratio, the better. A nonoccupant co-client on your loan means the lender considers both of your incomes when they look at how much you can get in a loan. Of course, you should be absolutely positive you can make the payments before you accept the loan. When they look at your application, lenders will also consider you and your co-signer’s debt-to-income ratio. Every lender has its own standards when it comes to what they consider an acceptable DTI. Knowing both your own and your co-signer’s debt-to-income ratio can make getting a loan easier.

U.S. Bank $50,000 Home Equity Loan

But you've got the knowledgeable WalletHub community on your side. Other consumers have a wealth of knowledge to share, and we encourage everyone to do so while respecting our content guidelines. In addition, it is not the financial institution's responsibility to ensure all posts and questions are answered. Before co-borrowing or cosigning a loan application, have an open conversation with the other person. Determine if the loan is necessary, consider what alternatives there are and discuss each person’s financial picture and future goals.

The process is quick and easy, and it will not impact your credit score. If you're ready to start comparing options, check out WalletHub's picks for the best personal loans with a cosigner and estimate your potential rates with the free pre-qualification tool. Cosigner services usually charge expensive fees, too, and can be prone to fraud. They don't have a great reputation either - for example, CosignerFinder has an F rating from the Better Business Bureau. All in all, it's not impossible to get a personal loan with no credit and no cosigner, but your options aren't the greatest either.

What are unconventional personal loans?

Your debt-to-income ratio is one of the most important factors that lenders consider when approving you for a mortgage. This number measures how much of your monthly gross income is used to pay your debt obligations, expressed as a percentage. For example, if you earned $6,000 per month before taxes, and you paid $2,100 a month for your student loan, car and credit card payments, your DTI would be 35%. Most lenders require a score of at least 680 in order to get approved for a home equity loan. However, you may still be able to qualify for a home equity loan with bad credit. Since home equity loans are secured by your property, meaning your home serves as collateral if you default on the loan, there’s less risk to the lender.

The lender considers both your income and your mother’s when they look at your application. Lenders also consider your mother’s finances, debt and credit when they look at your application, and decide to approve you for your loan. Although requirements vary, most lenders want to see a minimum credit score in the mid-600 range and a sizable percentage of equity in your home (usually 15% to 20%). Information provided on Forbes Advisor is for educational purposes only. Your financial situation is unique and the products and services we review may not be right for your circumstances.

$100,000 Business Loans

We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in oureditorial policy. Comparing home equity loan interest rates and terms online can help you find the right mortgage lender for you. Co-signing for a first or second mortgage loan does not automatically guarantee that you’ll be added to the home’s deed or title.

It’s not common for major personal loan providers to offer the option to apply with a cosigner, but there are a few good choices. To identify the best personal loans to apply for with a cosigner, WalletHub compared offers from the biggest personal loan providers that allow cosigners. Repaying debt on time adds positive credit history to your reports, which could raise your credit score over time. You may, for example, have better luck with a bank you’ve been with for years than with a company that only offers loan services. The amount you are eligible for will depend on several factors, including your employment or employability, educational background, financial behavior and credit history. Stilt does not disclose credit score, income or debt-to-income ratio requirements.

If you’re ready to apply for a personal loan with a cosigner, one of our featured lenders might be a perfect fit for you. Take your time while weighing your options, and apply with the institution most likely to meet your needs. The offers that appear on this site are from third party advertisers from which PrimeRates receives compensation.

All loans are subject to credit review and approval by our lender partners. When evaluating offers, please review the lender’s terms and conditions for additional details. By adding a cosigner's income and credit history to your loan application, you’ll drastically increase your odds of qualifying for attractive terms. In this way, the cosigner is leveraging their good credit to help you strengthen your own reputation as a borrower. It’s possible to apply for a first or second mortgage loan as a couple even if you’re not married.

For a jumbo loan, the minimum credit score required is 680, depending on the loan amount and the purpose of the loan. Set aside a monthly premium or two in your savings account in the event the primary occupant misses a payment. The interest rate is another critical component used when calculating your loan because even one tenth of a percentage point can add thousands of dollars to your mortgage over the years.

For example, if you have a credit score of 550 and limited income, you probably won't qualify for any worthwhile personal loans. But if you have a cosigner with an 800 credit score and a lot of income, you're likely to get a loan with very good terms. If you fail to make payments, you’ll hurt the cosigner’s credit, too, and they’ll be on the hook for paying. That could put a heavy strain on your relationship with the cosigner. In general, the best personal loans to get with a cosigner offer APRs as low as 5.99% and loan amounts as high as $100,000. Many of the best options also don’t charge origination fees, which helps to minimize the cost of the loan.

If your bank or mortgage lender offers home equity products, it might be more willing to work with you since you’re an existing customer, even if your credit isn’t up to par. For example, if you have a consistent history of making your mortgage payments on time, your lender might take that into consideration despite your credit. Before you agree to co-sign on a mortgage loan, it’s important to understand the legal and financial liability you’re assuming. As a co-signer, you’re agreeing to take responsibility for the loan if the primary borrower fails to make payments. You may have a co-signer on personal loans, student loans and auto loans as well.

No comments:

Post a Comment